Press Release

FOR IMMEDIATE RELEASE

Three markets claim three quarters of lab-construction completions in 2024: Boston, San Francisco, San Diego

Dallas – Jan. 10, 2024 – The U.S. life sciences real estate market faces multiple challenges this year, though the sector’s resilience is underscored by factors including increased federal funding, a growing pipeline of approved drugs and more corporate spending on research and development, according to CBRE’s 2024 U.S. Life Sciences Outlook.

Dallas – Jan. 10, 2024 – The U.S. life sciences real estate market faces multiple challenges this year, though the sector’s resilience is underscored by factors including increased federal funding, a growing pipeline of approved drugs and more corporate spending on research and development, according to CBRE’s 2024 U.S. Life Sciences Outlook.

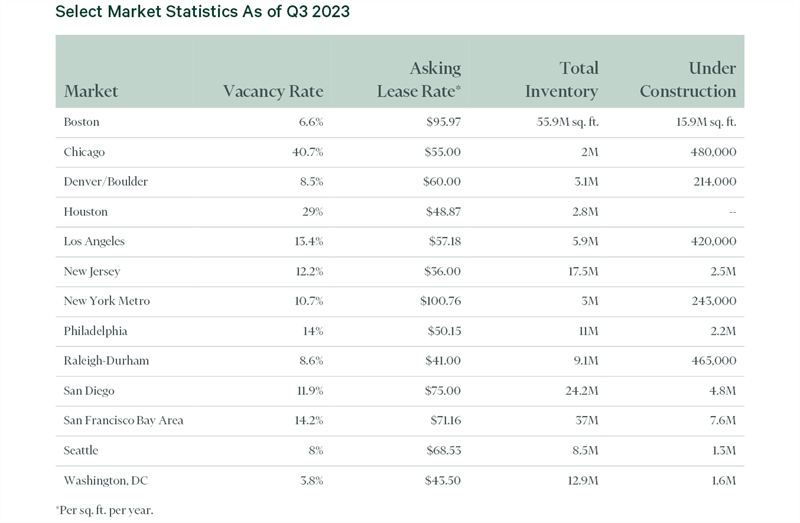

The life sciences real estate market will continue to moderate this year after rapid growth from 2020 to 2022 and a cooldown last year. CBRE foresees record construction completions of 21.3 million sq. ft. this year across the 13 largest U.S. markets, up from 13.9 million sq. ft. last year and 5.6 million sq. ft. in 2022. This year’s expected completions stand to push the 13-market average vacancy higher; it was 10.6% as of the third quarter of 2023.

Much of the life sciences sector’s slowdown can be attributed to the softer economy and a falloff in venture capital and initial public offerings. The sector’s once-surging job growth has slowed; CBRE forecasts a 0.2% decline in U.S. life sciences employment in this year’s first half, followed by mild job growth in the second half.

Despite those challenges, several factors bode well for life sciences. The U.S. Food & Drug Administration approved more novel drugs last year than in all but one of the previous 25 years, which foreshadows the need for more space for companies to refine, market and manufacture those drugs. Meanwhile, spending by public companies on research and development steadily increased over the past decade to nearly $180 billion last year.

A few sources of funding and equity are still growing, according to CBRE’s report. Funding from the National Institutes of Health stands at $47.8 billion, the largest budget to date. Philanthropic grants for life sciences research are increasing, though they’re a small portion of industry funding. And partnering arrangements are increasing between small, capital-needy drug developers and larger pharmaceutical companies.

“No doubt, 2024 will continue to see mergers, acquisitions and partnerships as the preferred strategic option given capital constraints and this interest rate environment,” said Matt Gardner, CBRE’s Americas Life Sciences Leader. “The underlying science still is strong following a decade of rising investment, as shown by recently robust levels of drug approvals and early-stage clinical trials. Construction completions will peak this year and then drop off substantially, benefiting the life sciences real estate market.”

CBRE’s analysis found that most of the construction set for completion this year – a 79% share – is in the three largest biotech hubs: Boston, the San Francisco Bay Area and San Diego.

To read the full report, click here.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2022 revenue). The company has approximately 115,000 employees (excluding Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves a diverse range of clients with an integrated suite of services, including facilities, transaction and project management; property management; investment management; appraisal and valuation; property leasing; strategic consulting; property sales; mortgage services and development services. Please visit our website at www.cbre.com.

Contact:

Kris Hudson

+1 214 863 3650

kris.hudson@cbre.com

The full content of this article is only available to paid subscribers. If you are an active subscriber, please log in. To subscribe, please click here: SUBSCRIBE