By eporter on January 25, 2023

Change in benchmark interest rates

|

|

|

|

|

|

|

|

|

|

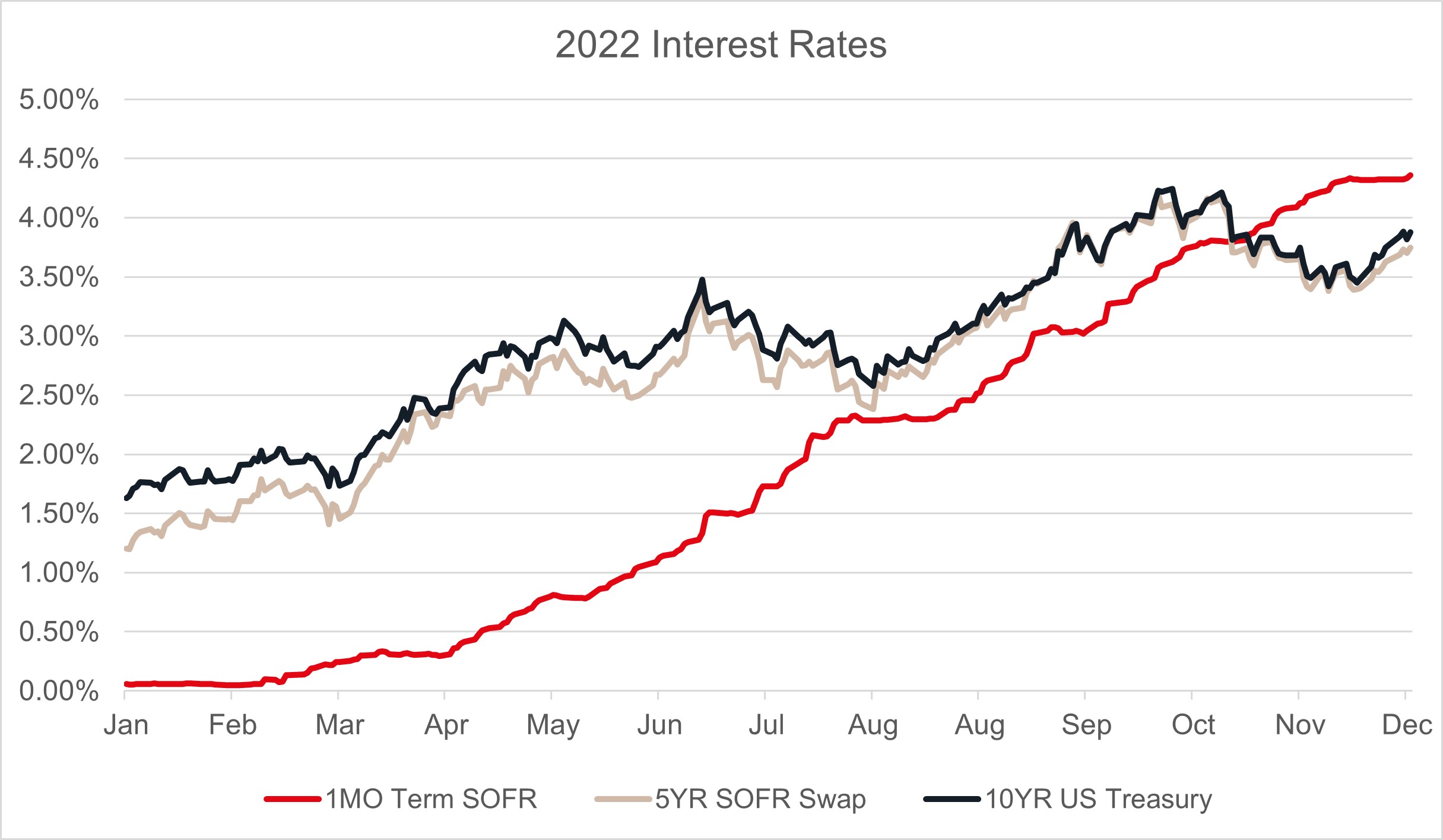

| · 2022 was a watershed year with rising interest rates which were at historically low levels in the last decade. Floating rate benchmarks increased 4.36% in 2022 and, importantly for medical office lending, 5-year swap rates increased more than 2.00%. The divergent trend in these rates led to an inverted yield curve which is impacting decision-making by borrowers on optimal loan structures and interest rate hedging strategies. Interest rate caps, a favored hedging tool in the recent past, became substantially more expensive. A 3-year SOFR cap with a 4% strike rate costs more than 3% of the total loan amount today.

· Other changes in loan economics and terms contributed to lowering sale prices and borrower behavior. Credit spreads widened overall due to economic uncertainty and other competitive factors, compounding higher nominal loan interest rates. With loan coupons 2 to 3 times higher than in 2021, the level of loan advances against property value were reduced by 15 to 20%. Debt service coverage was revived as a limiting factor for loan underwriting on the heels of the ultra-low rate environment.

· Medical office lending has unique characteristics that are supportive of the property sector overall. Loan availability has remained strong given the dominance by commercial bank / balance sheet lenders versus CMBS which is more important in other property sectors. Large loan underwriting, greater than $75 million, is hard to achieve today, creating an impediment to efficient execution on portfolio sales exceeding $100 to $150 million which dominated 2021 medical office sales volume. Large loans carry significant syndication risk as financing liquidity has become more challenging.

· The interest rate and debt market impact on medical office property values was dramatic in 2022. JLL calculates that, before accounting for changes in market sentiment, higher borrowing costs and lower leverage have mathematically impacted cap rates to maintain the same leveraged returns by at least 10%.

· Portfolio borrowing strategies, rate lock timing and knowledge of active lenders are a few areas where medical office borrowers need to navigate more artfully to maximize loan economics and take advantage of the pricing expansion. The JLL Healthcare Capital Markets debt specialists are well positioned to advise industry players, dissect the current markets and access a larger universe of lenders effectively. |

|

|

|

for $3.3B in 2022 closed healthcare capital markets transaction volume

|

|

|

|

$2B

investment sales & advisory and equity placement

|

|

|

165

properties

9.6B

square feet

|

|

|

|

|

Healthcare Capital Markets Contacts

|

Healthcare investment sales & advisory contacts

|

|

|

|

|

|

Healthcare debt advisory contacts

|

|

|

|

|

|

The full content of this article is only available to paid subscribers. If you are an active subscriber, please log in. To subscribe, please click here: SUBSCRIBE

Posted in Breaking News, Capital Markets, Companies & People, Thought Leaders