JLL Healthcare Capital Markets

Medical Office Perspectives

December 2020

W(h)ither monetization?

MOB buybacks by health systems consistently outpace monetization

Key points:

Key points:

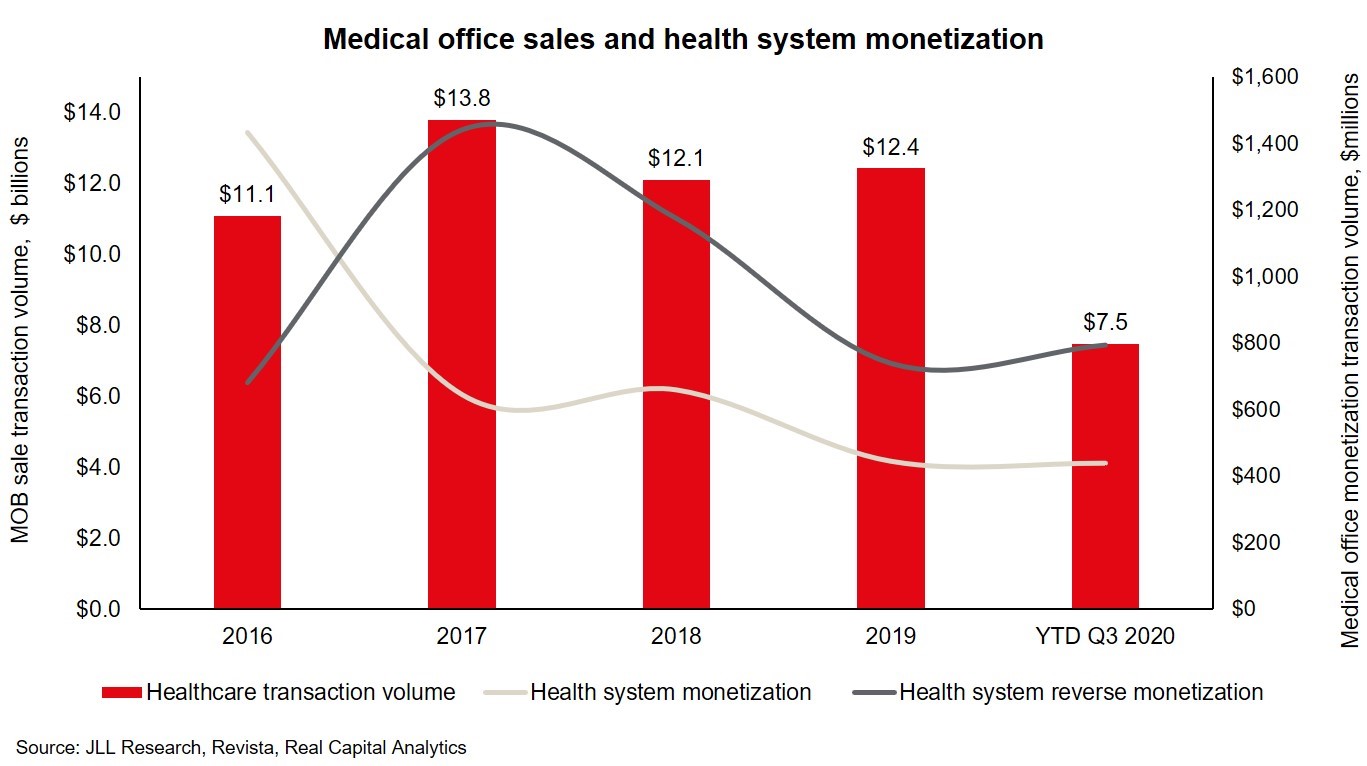

• Health systems are on track to buy $1 billion of their leased medical office buildings in 2020 between closed and announced transactions – a trend we’ve coined as “reverse monetization.” Despite the pandemic-related operating losses sustained by hospitals in 2020, health system liquidity remains high due to CARES Act funding and abundant access to capital. In fact, 2020 will be the third year in the past five during which MOB buybacks will exceed $1 billion, representing nearly 10% of all MOB trades. Buybacks typically occur when hospitals take advantage of purchase options embedded in leases or exercise contractual rights of first refusal. However, certain buybacks are happening today with no contractual rights.

• The popularity of MOB buybacks and ownership is fueled, in part, by the cash savings opportunity they create. During the pandemic, health systems are highly focused on reducing cash expense. MOB buybacks can eliminate rent payments and help cash occupancy costs. Health systems may also be able to avoid property taxes for qualifying properties – sometimes saving $3-4 per square foot. Even in the face of record high pricing for MOBs in 2020, health systems have been willing to pay top dollar – matching the most competitive real estate investors – in recognition of the significant bottom line advantage presented by buybacks.

• Where does the money come from to pay for buybacks? Hospitals’ cash reserves were fortified by the CARES Act, which bridged the initial loss of patient volumes and revenue. Today, most providers report that they are back to 90-95% of pre-COVID volumes, if not more, thanks to the reinstatement of elective procedures. Though operating cash flow has been significantly impaired in 2020, days cash on hand was less affected due to other sources of liquidity and the strong performance of investment portfolios for the not-for-profit health systems. Municipal bond issuance accelerated in 2020, increasing by 25%. Not-for-profit issuers enjoyed record low interest rates, which created cash interest savings for refunding bonds as well as new issuance. Thanks to nominal rates consistent with the direct cost of borrowing, many health systems have found structured finance products appealing to finance real estate, including credit tenant lease financing and synthetic leases.

• The headiest days of monetization date to 2016, when a record $1.4 billion of MOB sales by health systems occurred. Cash generated by sales of outpatient buildings, whether on or off campus, was used to reinforce liquidity, provide access to capital for high growth systems, transfer capital responsibility for buildings to a third party and manage regulatory compliance with physician tenants.

• Today, healthcare providers own 65% of MOB inventory nationally, down from 75% ten years ago, driven by the advent of new off campus outpatient clinics. Investor demand for medical office is at an all-time high, accelerated by the defensive qualities of the asset class and its proven durable performance. Investors can’t get enough MOB and now find themselves vying for investment alongside the tenants. Health systems face a happy decision – whether to buy or lease – with capital markets supporting them well, whichever choice they make.

Learn more about extracting capital from healthcare real estate in JLL: A 360 View of Healthcare Real Estate Monetization

Plus, view our 2020 Healthcare Real Estate Outlook>>

Recent 2020 activity

Closed – Investment Sale

Midwest Medical Office Portfolio

439,000 s.f.

Indiana, Illinois & Missouri

Closed – Investment Sale & Debt Placement

Greenpark II

80,098 s.f.

Houston, TX

Closed – Investment Sale

M.D. Medical Tower

68,285 s.f.

Midwest City, OK

Closed – Investment Sale

Lovelace Medical Center

69,539 s.f.

Albuquerque, NM

Closed – Debt Placement

Peachtree Orthopedics

60,578 s.f.

Cummings, GA

Closed – Debt Placement

San Juan Medical Center

42,970 s.f.

San Juan Capistrano, CA

Closed – Debt Placement

Milwaukee Nobis

20,383 s.f.

Milwaukee, WI

Contact us: JLLCapitalMarkets@am.jll.com

The full content of this article is only available to paid subscribers. If you are an active subscriber, please log in. To subscribe, please click here: SUBSCRIBE