JLL Healthcare Capital Markets Perspective

August 2019

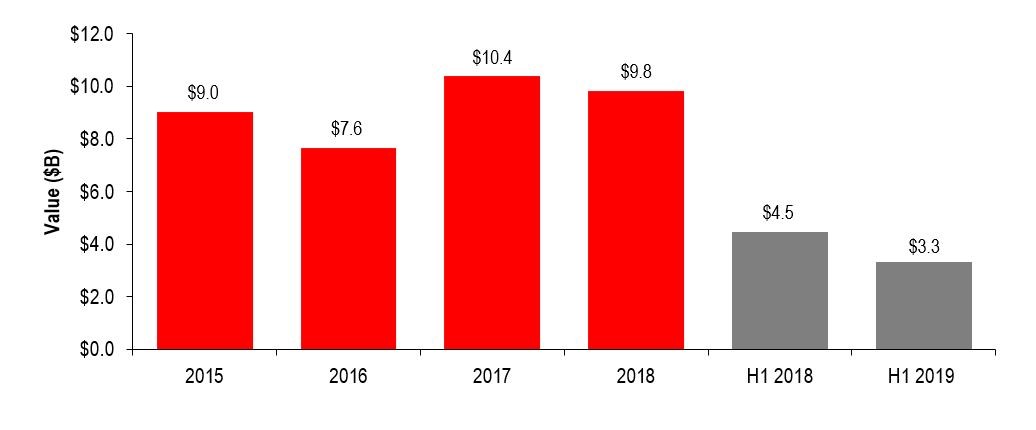

Medical office sales volume

Sales of all medical office buildings ≥ 25,000 s.f. (Source: Real Capital Analytics, JLL research)

Key points:

- The apparently lower level of medical office sales in the first half of 2019 belies the growing appeal of this historically “alternative” real estate asset class as well as portfolio sales that have transacted recently. Large portfolio sales (>$400 million) are an outsized portion of the story since 2017 representing roughly half of all sales, as investors and developers with large holdings took advantage of strong pricing levels to lock in superior returns. The first half of 2019 was no different and is best represented by the $1.25 billion CNL medical office portfolio sale (led by HFF Securities and HFF, before being acquired by JLL, who advised CNL on its sale to Welltower, Inc.). Waiting in the wings for the second half 2019 are several portfolios greater than $500 million that will drive overall 2019 volume, with reason to believe that 2019 will remain consistent with recent annual sales of $9 to $10 billion.

- The greater awareness and acceptance of the durable income characteristics of medical office has driven substantial capital raise for this sector – JLL is suggesting up to $5 billion of buying power – reinforced by the need for late cycle defensive plays in a challenging return environment. Healthcare is part of the wave of capital raise in niche sectors, notably outraising traditional real estate classes by 4 to 1. An uncertain economic forecast combined with low interest rates makes medical office’s higher and stable returns attractive.

- Demand is outpacing supply of quality product available for sale – the biggest challenge in the current environment – as 70% of medical office properties are still owned by healthcare providers that have been reluctant to monetize given their good access to capital. New construction represents only 2% of existing inventory and is similarly split with only 26% of projects underway with third party developers. The short-term effect is continued return compression for investors seeking to deploy allocations to acquire at market, yet still offering return premiums over hot sectors like multi-housing and industrial. Count on opportunistic owners of medical office – be they investors or providers – to respond to superior pricing levels and offer new supply to eager investors and new entrants.

The full content of this article is only available to paid subscribers. If you are an active subscriber, please log in. To subscribe, please click here: SUBSCRIBE