Included in this edition:

Included in this edition:

As Interest Rates Creep, Door Opens for Institutional Medical Investors

• U.S. Medical Office Building Construction Trends

• Notable Healthcare Real Estate Transactions from Last Quarter

• National Medical Office Cap Rate Trends

• National Medical Office Sales Volume

• Debt Market Update for Medical Properties

As Interest Rates Creep, Door Opens for lnstitutional Medical Investors

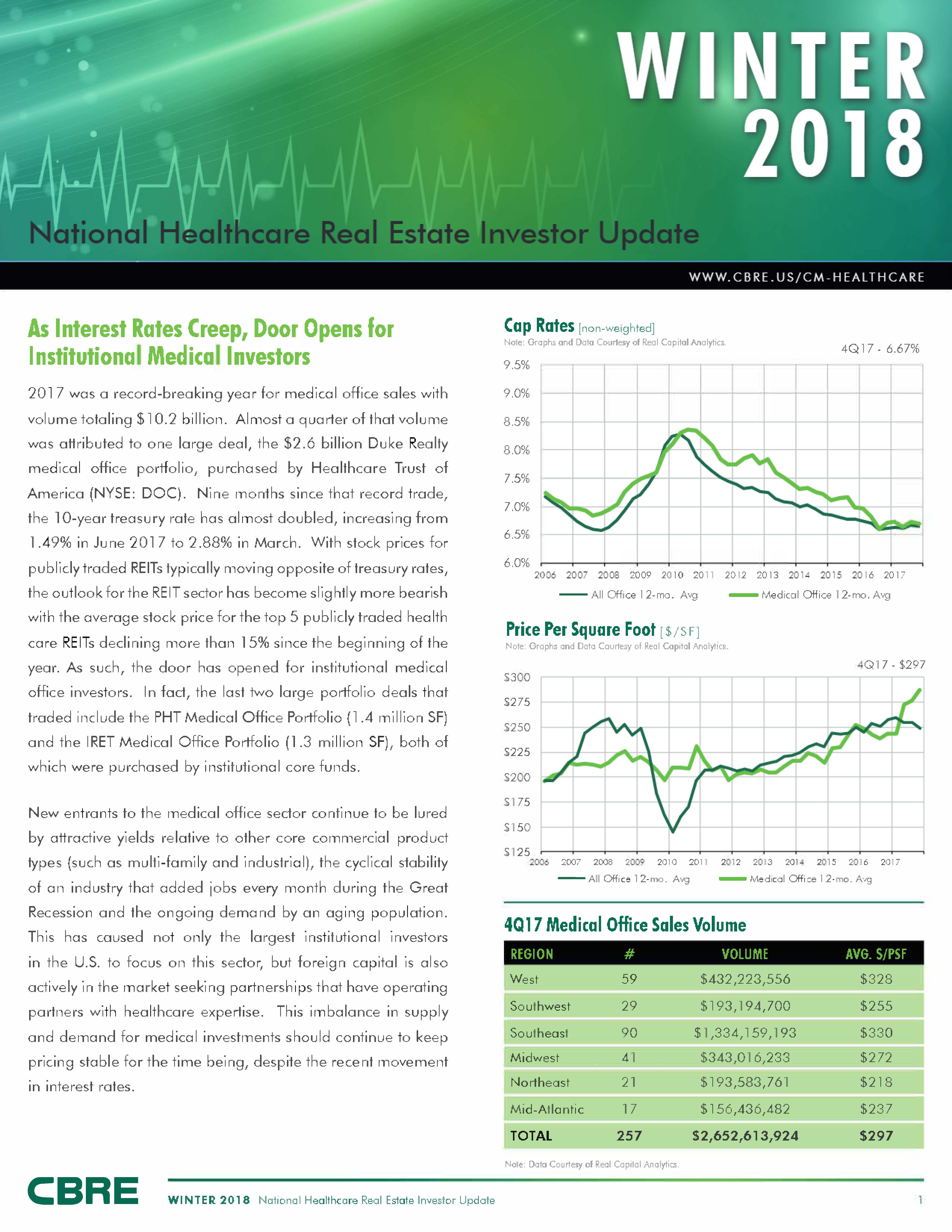

201 7 was a record-breaking year for medical office sales with volume totaling$10.2 billion. Almost a quarter of that volume was attributed to one large deal, the $2.6 billion Duke Realty medical office portfolio, purchased by Healthcare Trust of America (NYSE: DOC). Nine months since that record trade, the 10-year treasury rate has almost doubled, increasing from 1.49% in June 2017 to 2.88% in March. With stock prices for publicly traded REITs typically moving opposite of treasury rates, the outlook for the REIT sector has become slightly more bearish with the average stock price for the top 5 publicly traded health care REITs declining more than 15% since the beginning of the year. As such, the door has opened for institutional medical office investors. In fact, the last two large portfolio deals that traded include the PHT Medical Office Portfolio (l .4 million SF) and the IRET Medical Office Portfolio (1.3 million SF), both of which were purchased by institutional core funds.

New entrants lo the medical office sector continue lo be lured by attractive yields relative to other core commercial product types (such as multi-family and industrial), the cyclical stability of an industry that added jobs every month during the Great Recession and the ongoing demand by an aging population. This has caused not only the largest institutional investors in the U.S. to focus on this sector, but foreign capital is also actively in the market seeking partnerships that have operating partners with healthcare expertise. This imbalance in supply and demand for medical investments should continue to keep pricing stable for the time being, despite the recent movement in interest rates.

To download the complete report, please click here.

For more information, please contact:

U.S. HEALTHCARE CAPITAL MARKETS GROUP

CHRIS BODNAR

Vice Chairman

Investment Properties

+1 303 628 1711

chris.bodnar@cbre.com

LEE ASHER

Vice Chairman

Investment Properties

+1 404 504 5965

lee.asher@cbre.com

RYAN LINDSLEY

Senior Director

Investment Properties

+1 303 628 1745

ryan.lindsley@cbre.com

SABRINA SOLOMIANY

Senior Director

Investment Properties

+1 404 536 5054

sabrina.solomiany@cbre.com

The full content of this article is only available to paid subscribers. If you are an active subscriber, please log in. To subscribe, please click here: SUBSCRIBE